The basic process of green field innovation is one of expanding the field of possibilities and then narrowing it down or at least prioritizing the possibilities.

Throughout this post, I'll use the insurance industry and a fictional company called Remote Employees Insurance Company (REICO). We'll also apply a constraint and assume our upper management has insisted that the greenfield we explore must involve online payment innovations because investors are excited to explore this realm. My ignorance of all of the above will will force me to stick to general principles.

Here's a cheat to help you jump to the parts you care about.

- Understand the Field of Play

- Understand the Rane of Pain Points

- Understand the Range of Opportunities

- Identify Overlap

- Prioritize Possibilities for Experimental Development

- Set Metrics

- Measure Success

- Expand, Pivot, or Start Over

- Onward

Understand the Field of Play

To my knowledge and based on my research, REICO insures or manages insurance policies in a variety of fields including, approximately:

- Auto insurance

- Homeowner’s, condo, mobile home, and renters insurance

- Umbrella insurance policies

- Flood insurance

- Boat, RV, ATV, motorcycle, recreational vehicle insurance packages

- Commercial vehicles

- Rideshare insurance

- Pet Insurance

There may be more, but this gives us a good sample.

Understand the Range of Pain Points

Pain points can be, among other possibilities, specific hurdles to adoption, longitudinal or recurring friction, or internal costs and inefficiencies. Some example pain points that REICO might be facing include

- Complex billing structures and payment reconciliation. Almost inevitable given the number of fields REICO insures in.

- Manual processes. Many insurance providers still rely on manual payment processing methods, leading to inefficiencies, errors, and delays in payment posting and reconciliation.

- Regulatory compliance.

- Payment and claim fraud.

- Customer expectations. Policyholders expect convenient, user-friendly payment options. They will leave because of a poor UX experience.

- Data security. REICO has a massive amount of sensitive and regulated user data, including payment information, making it an attractive target with a lot to lose.

- Multi-channel payments. Clients may wish to pay through app, phone voice-operated system, paper checks, or direct drafts. Worse, clients may wish to make partial payments through different channels.

- Regulatory changes. There is a need to stay tuned to updates to the Payment Card Industry Data Security Standard (PCI DSS) or state-specific billing regulations.

- Customer communication. Customers become concerned over poor communication especially when money is involved.

- Transaction volume.

Understand the Range of Opportunities

There have been a lot of exciting developments in the online payments space over the last few years. Some example opportunities that REICO might tap in the payments space might include:

Payment methods

- Accepting or providing digital wallets

- Contactless payments

- Voice-Activated Payments

- Cryptocurrency payments

Security

- Biometric authentication

- Tokenization

- AI for fraud detection

Financing as a Service

- Buy Now, Pay Later (BNPL)

Payments Integrations

- API connectivity with banking and budgeting software

Identify overlap

Here we look at our enterprise’s strengths, weaknesses, opportunities, and threats. The different fields of play will present different problems and opportunities. For instance:

- Pet insurance will require much smaller and more frequent payments than homeowner’s insurance requires. Those payments will probably not be managed by a third party in the way a mortgage bank collects the homeowner’s insurance premiums as part of its monthly drafts.

- Car insurance premiums can be a jolt for some clients’ finances. Many insurance companies offer to break apart those premiums into two or three payments. Integrations with budgeting software or buy-now-pay-later programs may help ease these payments for those insureds.

- REICO has, through agents, some brick-and-mortar presence. Introducing contactless payment at those locations or at partner locations could improve revenue recognition or client retention.

- API-based connectivity with voice-connected systems such as Alexa or Google Home and Google Calendar could provide easier reminders and prompts for people to pay their premiums in a more convenient way.

- All online payment systems are subject to fraud. Improving security is always in-season. Especially valuable right now would be improved authentication (biometrics or other passwordless technology) and AI for at-scale fraud detection.

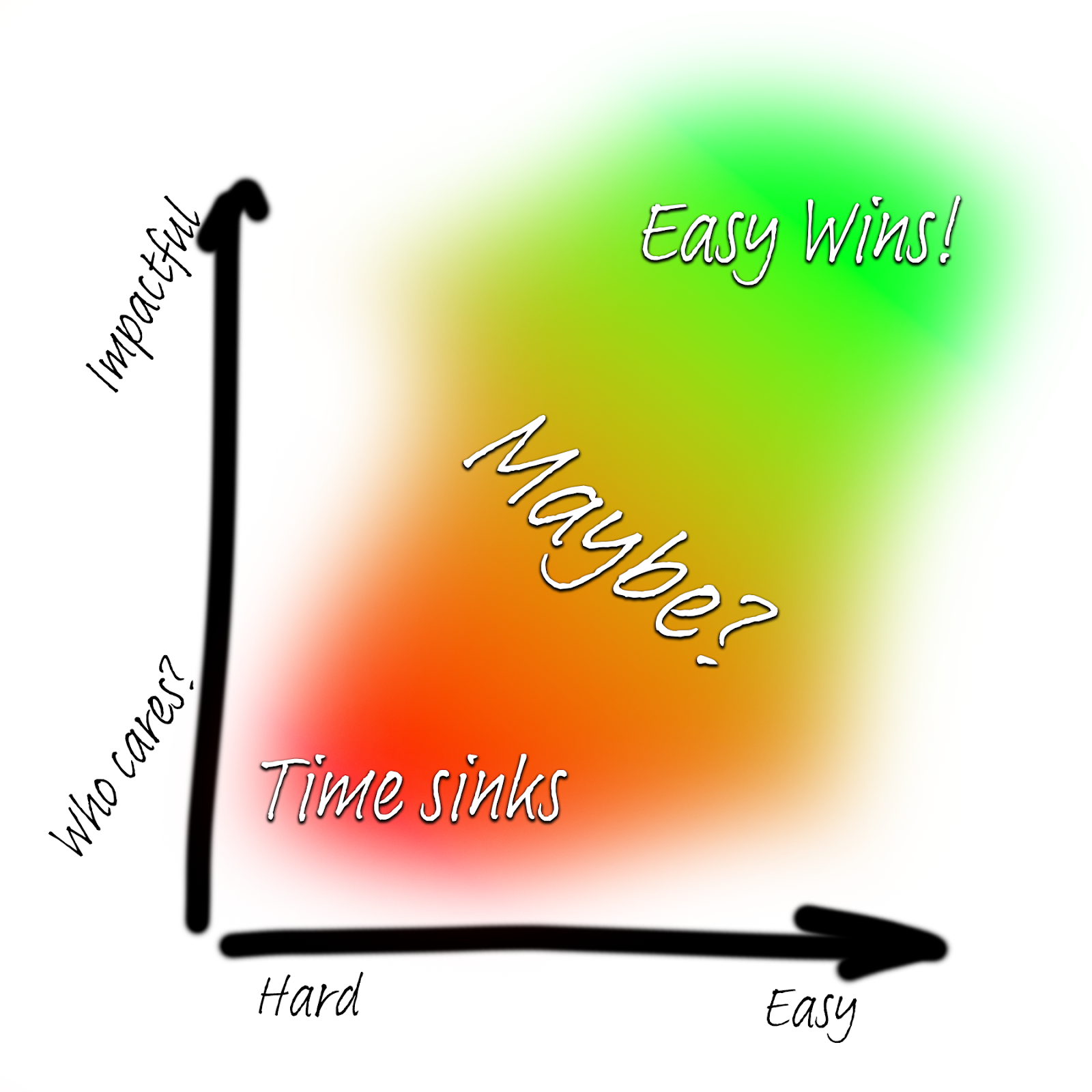

Prioritize Possibilities for Experimental Development

Once we’ve brainstormed a list of possibilities, we should start narrowing down or, better, prioritizing them based on likely return on investment.

I generally recommend prioritizing building based on level of impact versus level of effort or ease of effort.

In this section, we're going to look at the general principles of prioritizing so that you can apply them to your API or other product scenario.

I measure impact in terms of revenue gained or retained and in terms of costs incurred versus costs saved. I try to do this in terms of dollars and cents as close as possible, though I admit up front that usually, the best one can do is something pretty fuzzy. If you do your estimating even in a fuzzy way, you'll at least have a rational, defensible decision rather than gut impulses and intuitions.

Risk assessment is also important. There are risks involved both in adopting and in declining to adopt different features and capabilities. When possible, these should be estimated as quantities and weighed with impact.

At a high level, you "divide" revenue or cost improvements by the level of effort for any particular bit of work. You get a ratio then and can identify, at least approximately, the possible developments that will have a large positive impact at a low cost. These are the easy wins that should make your heart sing and that you should prioritize.

As part of prioritization, we want to look at metrics that will reliability predict impact.

Set metrics

Because our goal is to increase profit by (a) increasing revenue, (b) reducing costs, or (c) both, our KPIs after the fact are always going to come down to attributable revenue growth or cost reductions. The problem is that these metrics only tell us if our green field venture has worked. We’d like be able to make reasonable predictions about whether it will work or is working so that we can pivot before sinking too much cost.

The key thing about a leading indicator is that it should reliability predict the thing we care about, profitability. For this, we want to make a good study of our business’s and industry’s data.

Insurance may be one of the very original subscription models, and it shares a key metric of profitability with Saas software: customer retention.

Another key indicator that software innovations can impact is the expense ratio, the proportion of earned premiums that is eaten away by operating costs and inefficiencies whether that means payroll, security, or liabilities that arise. If we can identify, for instance, that a software innovation like a customer support chatbot reduces customer support calls by X%, we can expect savings as a function of X.

If we have decided to adopt AI to help with fraudulent payment detection, we want to look at the number of fraudulent payments and the cost to resolve each one. In this case, a strong leading KPI would be the number of fraudulent payments detected minus the number of false positives requiring human intervention.

We can use these predictive KPIs to measure the effect of our developments.

Measure success

Measuring success is tied together with rollout. There is a temptation to roll out a new feature or innovation across one’s customer base with a big splash. The problem is that big splashes can cause lots of damage.

SaaS software companies have become more conservative in their rollouts over the years, rolling out changes first to small groups of eager, early adopters, then to larger and larger subsets of their customer base before finally making the new features standard or mandatory.

Going back to our example of AI fraud detection, we might roll it out to our 10% most stable customers as an opt-in program. From this, we can get data about:

- How willingly long-term, valued customers will adopt this technology, possibly extrapolating from there to less stable customers

- Fraudulent payments detected

- False positives

- Effects on retention

- Customer feedback

This data will be very valuable for helping us decide whether to expand the program, re-define it, or cut it altogether.

Expand, pivot, or start over

The decision to expand, pivot, or start over is multivariate. Factors include

- KPIs and profitability. Did the KPIs measure as hoped for, and has this translated to profitability?

- Cost-benefit analysis. Is the ROI there?

- Customer and stakeholder feedback. Are there suggestions for a pivot that could lead to improvements?

- Competitor analysis. Just like we analyze the competition at the start of a new endeavor, it is worth revisiting the competitor afterward. It may be that what was once an innovation has become table stakes in our market and we must maintain the feature regardless of cost.

- Finally, is there something we can do that is more profitable with the same resources?

Sticking with our example of adopting AI for fraudulent payment detection, we might see

- A 1500% increase in the number of correct, verified detections, which at REICO's scale could save significant associated costs.

- A 50% in the number of false positives. A false positive may be much more expensive than an undetected fraudulent payment because of associated friction and churn of customers annoyed by the inconvenience.

- A 3200% increase in customer support cases associated with payments.

- Even though AI-based fraud detection isn’t a feature offered to customers, it may be considered table stakes because of insistence by executives, investors, business partners, or even regulators.

In the scenario above, because the numbers are so mixed, but the basic need is so strong, the best approach would probably be a pivot. The pivot may involve fine-tuning the technology, turning to a different AI technology, applying the tech to a different segment of our customer base, or adopting other technologies like chatbots to reduce the friction created by this adoption.

Onward

Greenfield product investment within an enterprise is a lot like starting a whole new enterprise, a whole new startup. There is risk. With the risk there is opportunity. Careful bet-hedging and risk monitoring can reduce the risk and signal the time to pivot to new opportunities. Much of my thinking in this post has been inspired by Eric Ries's The Lean Startup. If you want to dive into any of the preceding topics, I can't recommend a better text for getting started.